A New Dallas

Economics

Unlike when it was first built, there is no new economic development to be gained from rebuilding the highway. For the most part, when it was first built, much of the benefit went outside of Dallas city limits following the highways to the virgin land they unlocked. From now on, in perpetuity, IH345 is an on-going cost simply to maintain it and keep it from falling down.

In terms of repairing it or rebuilding IH-345, no funding has yet to be identified. TxDOT is $17 billion in debt. The federal Highway Trust Fund pays for 90% of a new highway’s cost, but not as much for the maintenance or replacement of existing highways. Public coffers are empty. Sprawl emptied them. Rather than spend public money toward zero gain, this study proposes the conveyance of public right-of-way land to new parks and private development in order to reduce TxDOT’s maintenance costs while alleviating debt. In exchange, the city gets investment and new tax base. The citizens get increased housing choice in highly desirable in-town areas with true transportation choice. Investors and developers get new opportunities in prime location for development and profit.

Existing Condition: After reviewing every property within the 245-acre study area, it was discovered that there is only $19,906,970 in improvements throughout the site. This equals a little over $81,000 per acre (less intense than most sprawl). Furthermore, the city only generates $3,584,832.20 in annual property tax revenue.

Pro Forma: 9 locally comparable areas were used to model 9 different development scenarios in the pro forma. If the development is able to achieve similar levels of density and land value as CityPlace (meaning primarily residential, mostly low- and mid-rise with some high-rise), the city would see $4,060,663,220 in investment over 15 years, assuming 95% absorption at year 15. This equates to yearly property tax revenue of $110,043,972 for the city of Dallas. Or enough to implement the entire bike plan and run modern streetcar lines from West End to Lower Greenville and Union Station to Exposition. In one year of revenue. The investment community believes the city of Dallas could borrow $1 billion against the new revenue generated by this project.

Before

Improvements: $19,906,970

Annual Property Tax Revenue: $3,584,832

After

$4,060,663,220 (204x greater)

$110,043,972 (30x greater)

Cost: TxDOT has not yet priced any of their options. As that information becomes available, it will be posted here. However, as the previous section pointed out there is no new economic benefit for that cost. However, by spending to remove the freeway, both the city and state, and their constituents, would see significant gains.

Based on cost of demolition from similar highway tear-outs around the country, prorated based on inflation and length of highway segment, it would cost an estimated $55-65 million to demolish the 345. According to our projections, that equates to more than a 60-to-1 return on investment. Furthermore, it would cost another approximated $11,270,000 to build the grid of streets in the highway’s place. However, much of this can be offset by the four (4) TIF districts currently in place overlapping various portions of the study area.

Absorption:

Suburban competition: As Jeff Speck wrote in Walkable Cities, while cities are in competition with each other, they are more at competition with their suburbs, “yet they don’t know it.” To help illustrate this point, the city of Detroit’s population plummeted between 1950 and today, dropping from 1.85 million to 770,000. However, the metropolitan area grew during that time span from 3.3 million to nearly 5 million.

The Dallas-Fort Worth Metroplex is the fastest growing region in the country. Between the 2000-2010 census, the metropolitan area grew from 5.16 million to 6.37 million people. However, this explosive growth coincides with stagnation for the city of Dallas. The city of Dallas grew by only 9,236, garnering but 0.7% of region-wide population growth. The last time Dallas gained so few people was between 1870 and 1880 when Dallas grew from 3,000 to 10,358.

Density equals desirability. And to gain population, we can’t move cars, but we have to instead move the market… to favor infill development.

Lack of infill housing: To further underscore the point that the development market is still sprawling outwards to the detriment of every city in the metroplex, according to a 2012 EPA survey of new housing developments between 2000-09, only 17.2% of new housing was in infill locations within all of DFW. Meaning, over 80% of new housing units were built at the bleeding greenfield edge of sprawl, requiring all new infrastructure.

To put that in context, here is the top 10 of metropolitan areas in terms of percentage of housing in infill locations, i.e. the upgrading of existing areas:

1. San Jose, 79.7%

2. Los Angeles, 62.6%

3. New York, 60.8%

4. San Francisco/Oakland, 56.2%

5. Portland, 44.3%

6. Miami/Dade, 42.5%

7. Chicago, 41.1%

8. Seattle/Tacoma, 39.8%

9. San Diego, 38.2%

10. Boston, 31.3%

Of these, only DFW and Portland declined in percentage of infill between 2000-05 and 2005-09.

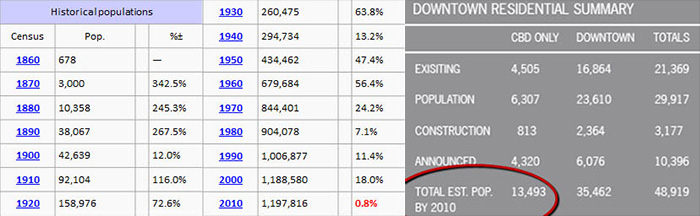

Downtown Falling Short of Projections: While downtown Dallas has experienced a renaissance since 2000, much of which it could be argued is through the benefit of DART’s introduction, reconnecting downtown to its surrounding areas. However, its growth has slowed nearly to a halt.

A 2006 study, when the population of the downtown central business district was 6,307 projected 13,493 residents by 2010. By 2013, that number is 7,400, just 15% of the projected growth. The fundamental problem facing downtown Dallas, that this effort is intended to reverse, is that the real estate market in downtown is “upside-down.” Demand is too low and land costs are too high, all expecting the next high-rise condo tower to drop from the sky. Cities are ultimately engines of value creation. They wouldn’t exist if they didn’t create profit, be that economic, social, or environmental.

Much of the new investment in downtown is also not market-oriented. This is impossible to sustain. To fully revive downtown Dallas, we must pursue market-based strategies such as opening up public land put to detrimental use for private investment towards the greater good.

Capturing Pent-up demand: Based on national surveys conducted by Christopher Leinberger of the Urban Land Institute, 40% of the entire country wishes to live in a walkable neighborhood. Only 3% actually does. In his study in collaboration with the George Washington University’s School of Business WalkUP: Wake Up Call,” Leinberger demonstrates a correlation between walkscore and property value. In fact (though this study was conducted only in DC metro), for a 6 point increase in WalkScore, rents for office, retail, and residential uses also increased $6-7/sq.ft.

In Dallas, there also is an extreme pent-up demand for walkable urban housing. The few walkable locations have significantly inflated rents compared to their surroundings. By creating high quality walkable, urban housing immediately adjacent to downtown will ultimately yield more affordable walkable and transit-oriented development.

Furthermore, the Millennial generation now entering the work force is as large as and will have as much of an impact on our physical environment as the Baby Boomers. Of these 80 million from 18-35 year old future “job creators,” 77% desire interesting, walkable urban areas. In the DFW area, only about 1.5% currently live in walkable neighborhoods and 4.5% of those in Dallas proper.

INFRASTRUCTURALLY COERCED CAR OWNERSHIP: We like to think our vehicle sets us free. However, how many of your daily destinations can legitimately be reached in a safe and comfortable manner without a car? Again, this is a direct by-product of an infrastructure network that limits available mode or route choice. The smartest cities empower its citizenry with choice, the ability to make the appropriate decision based on changing circumstance. This lack of choice makes the city of Dallas exceptionally fragile and susceptible to any disruption…

It is also an incredible strain on the local economy, beyond the public cost of infrastructure and the injuries caused by it. It is also costly on a household by household basis. Based on national average cost to own and operate a car per year of $8,946.00, if HALF the 343,000 households in Dallas County with 1 car could give up their car, and HALF the 321,000 households with 2 cars could give up 1 car, and every household of more than 2 cars could give up 1 car, that equates to 466,000 less vehicles owned by Dallas residents. That is a drop of 31% in total ownership. It also equals $4,168,836,000/year that would stay in the local economy by way of better housing, small business investment, additional spending, or savings.